10 Things You Should Know Before Getting Home Insurance

Buying a house is probably the biggest investment you’ll ever make.

Anybody buying a house for the first time in the suburbs or an experienced homeowner looking to switch insurance companies in 2026 may find it hard to understand how complicated home insurance is.

It isn’t just about finding the lowest premium; it’s about ensuring that your sanctuary—and your financial future—is protected against the unexpected.

To help you make an informed decision, here are ten essential things you must know before signing on the dotted line for a home insurance policy. ” Home Insurance “

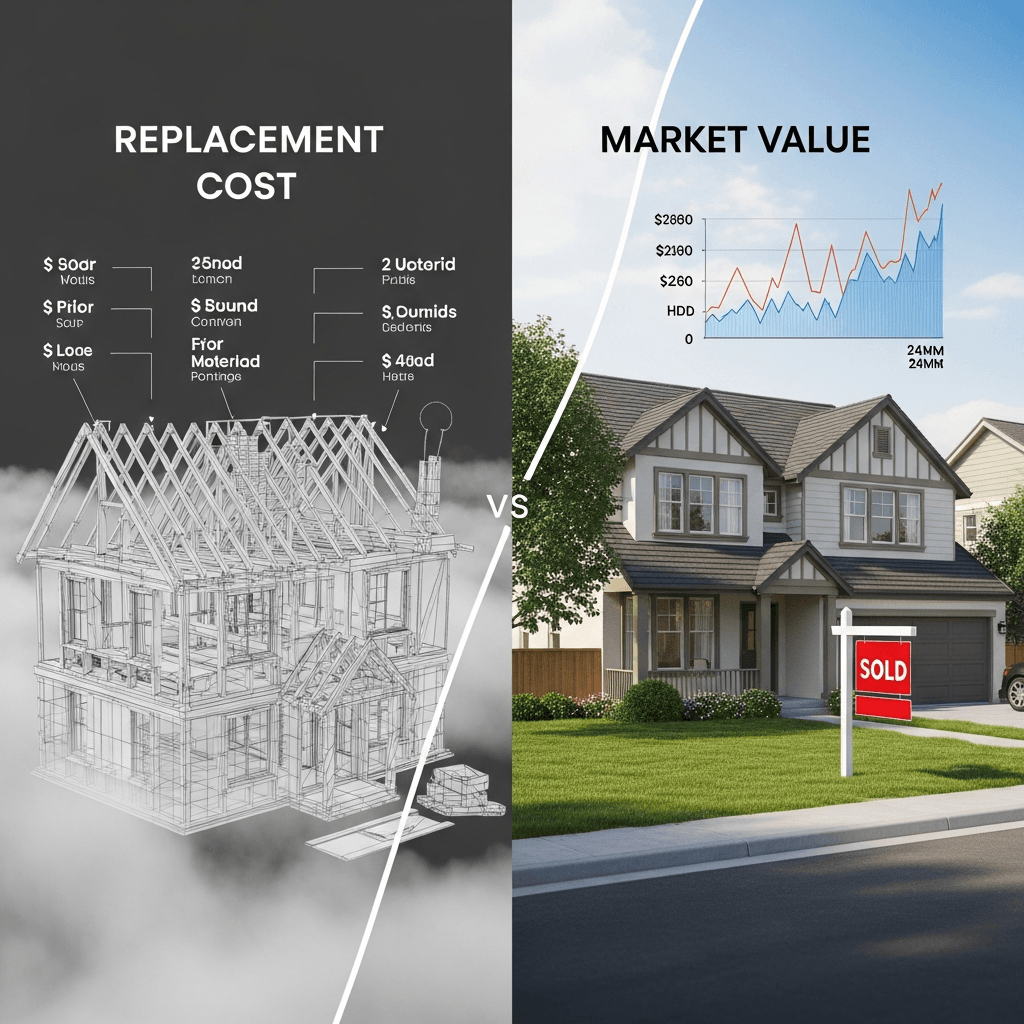

1. Replacement Cost vs. Market Value

One of the most common mistakes homeowners make is insuring their home for its market value (what you could sell it for). However, insurance is designed to cover the replacement cost—the actual dollar amount required to rebuild your home from the ground up at today’s prices for labor and materials.

- Why it matters: In 2026, construction costs have fluctuated due to supply chain shifts and labor shortages. If your home is insured for its $500,000 market value but costs $650,000 to rebuild due to local building codes and material costs, you could be left with a $150,000 deficit after a total loss.

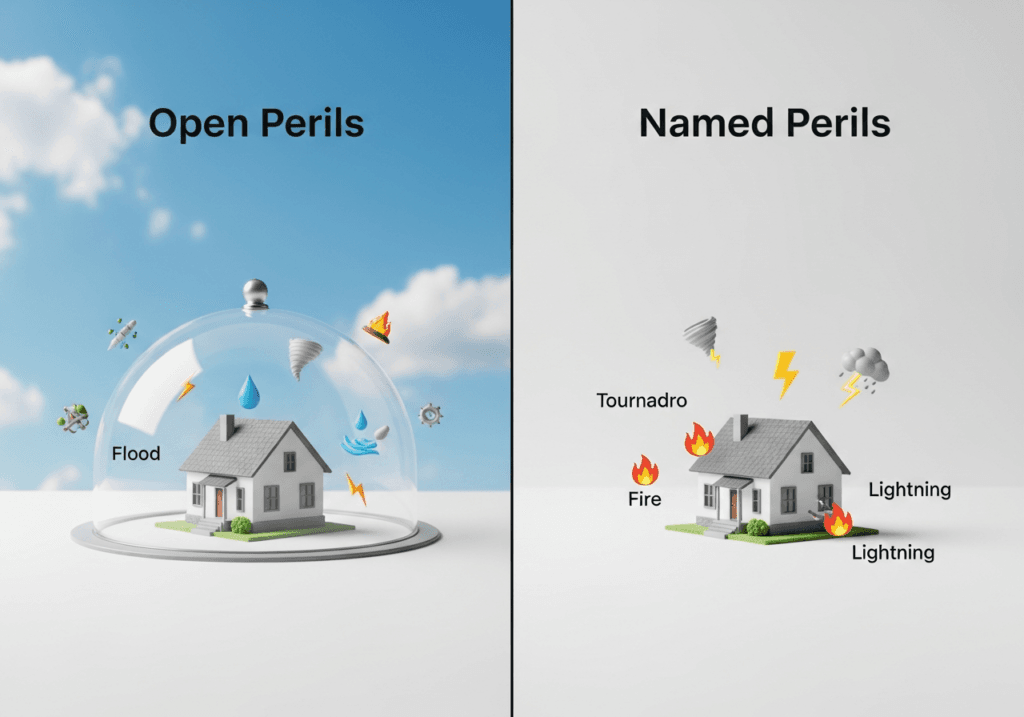

2. The Difference Between “Open Perils” and “Named Perils”

Not all policies are created equal. You need to know which “perils” (events like fire, wind, or theft) are covered.

- Named Perils (HO-1 or HO-2): Only covers specifically listed events. If it’s not on the list, you aren’t covered.

- Open Perils (HO-3 or HO-5): This is the gold standard. It covers everything except for a few specific exclusions listed in the policy (like war or nuclear hazard). Most modern homeowners should aim for an HO-3 policy at a minimum.

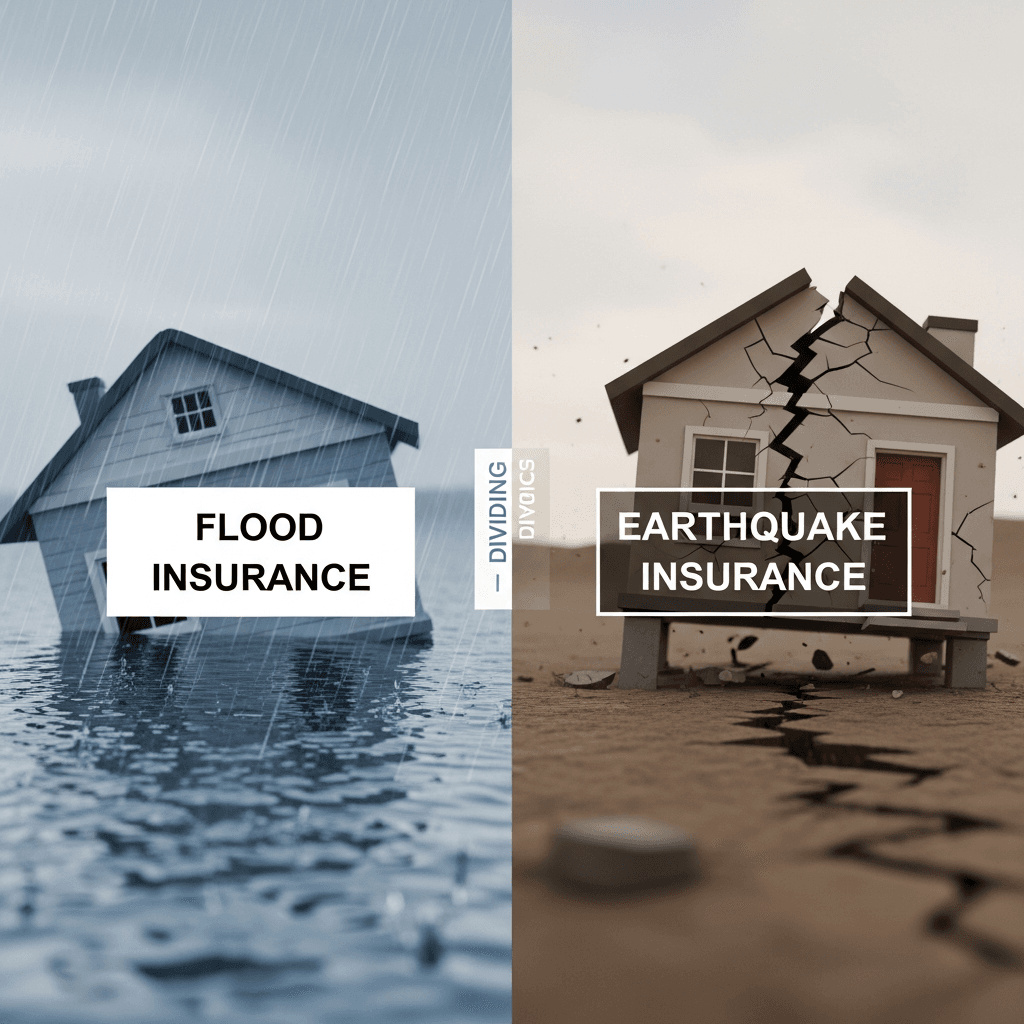

3. Flood and Earthquake Insurance are Separate

A standard homeowners policy almost never covers damage caused by floods or earthquakes.

- The Reality: Even if you don’t live in a high-risk “flood zone,” localized heavy rainfall or a burst water main can cause rising water damage that a standard policy won’t touch. You must purchase a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private insurer to stay protected.

4. Your premium is affected by your credit score.

- Across a multitude of jurisdictions, insurers implement a “Credit-Based Insurance Score.” According to actuarial data, individuals who effectively manage their credit are more likely to submit fewer claims.

- The Takeaway: Before shopping for insurance, check your credit report. Correcting errors or paying down a small balance could potentially save you hundreds of dollars on your annual homeowners’ premium.

5. Liability coverage serves as your financial safety net.

Home insurance is not limited to protecting your assets from litigation; it also protects your physical structure.

Liability coverage pays for legal defense and settlements if someone is injured on your property or if you (or your family members) accidentally damage someone else’s property.

- 2026 Strategy: With legal costs rising, the standard $100,000 liability limit is often insufficient. Most experts recommend at least $300,000 to $500,000. If you have significant assets, consider an Umbrella Policy for an extra layer of protection.

6. The “CLUE” Report Follows the House (and You)

Insurers check a database called the Comprehensive Loss Underwriting Exchange (CLUE). This report lists all insurance claims filed on a specific property over the last five to seven years.

- Why check it?If the property you’re purchasing has a history of water damage or broken pipes, your rates may be higher, or the insurance company could not cover it at all until the repairs are confirmed.

- Always ask the seller for a copy of the CLUE report during the inspection period.

7. Deductibles: Fixed vs. Percentage

Most people are familiar with a flat deductible (e.g., $1,000). However, many policies now use percentage deductibles for specific risks like wind, hail, or hurricanes.+1

- The Math: If your home is insured for $500,000 and you have a 2% windstorm deductible, you will have to pay $10,000 out of pocket before the insurance kicks in. Always check the “fine print” on your declarations page to avoid a massive financial surprise after a storm.

8. Actual Cash Value (ACV) vs. Replacement Cost on Contents

Just as with the structure, your personal belongings (furniture, electronics, clothes) can be insured in two ways.

- ACV: Pays what the item is worth today (depreciated value). That 5-year-old laptop might only get you $100.

- Replacement Cost: Pays what it costs to buy a new version of that item today. While this coverage is slightly more expensive, it is almost always worth it when you have to refurnish an entire home after a fire.

9. High-Value Items Require “Scheduling”

Standard policies have “sub-limits” for certain categories of items. For example, a policy might cover $1,500 for jewelry or $2,500 for silverware.

- The Fix: If you have an engagement ring worth $10,000 or a high-end art collection, you need to “schedule” these items individually. This involves getting a professional appraisal and paying a small additional premium to ensure they are covered for their full, specific value.

10. Maintenance is NOT Insurance

This is perhaps the most important lesson for any homeowner. Insurance is designed for “sudden and accidental” damage. It is not a maintenance contract.

- Example: If a 20-year-old roof leaks because it was never replaced, the insurer will likely deny the claim, citing “wear and tear.” Similarly, slow leaks that occur over months (like a dripping pipe behind a wall) are often excluded. Regular home maintenance is the only way to protect yourself from these out-of-pocket expenses.

Final Thoughts: Shop and Bundle

To get the best value in 2026, don’t just settle for the first quote you receive. Use an independent agent who can shop across multiple carriers. Additionally, “bundling” your home and auto insurance with the same company remains one of the most effective ways to secure a 10% to 20% discount on both policies.

By understanding these ten pillars of home insurance, you move from being a passive policyholder to an empowered homeowner.You’re not simply purchasing a piece of paper; you’re buying the peace of mind that your house will always be safe.